Bootcamps are Dying: Is Higher Ed Next?

and GenAI hiring + job apps, Druckenmiller's dedication, and amping it up

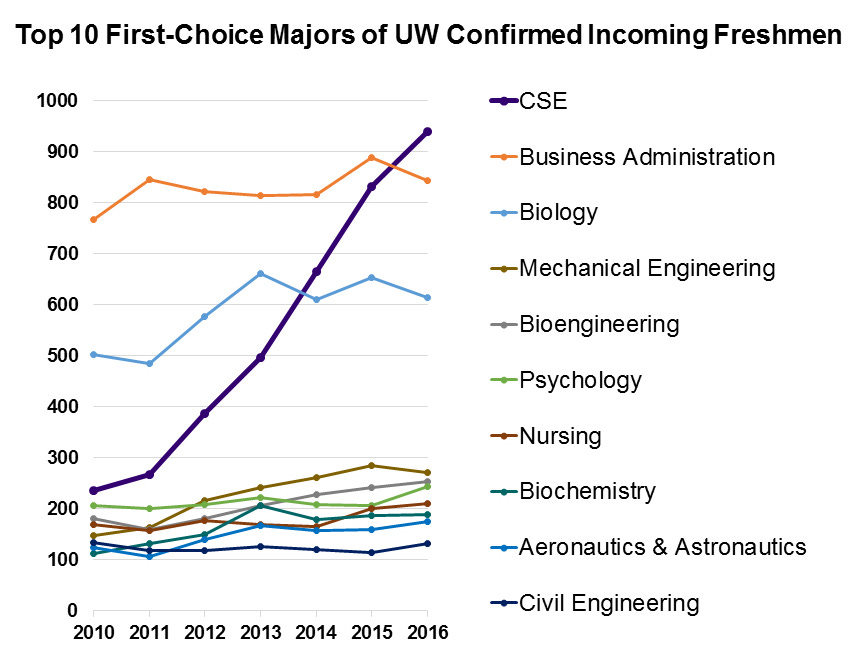

Want to know who ruled UW’s college campus back in 2015?

Here's a hint: it wasn't the football team. It wasn't the business majors with their pressed suits. And it definitely wasn't the fraternity presidents who denied me entry to their parties.

It was the computer science and computer engineering majors. Getting into the University of Washington's CSE program required a 3.8 pre-requisite GPA to have a shot at declaring the major. And once you got in? You were basically royalty on campus.

As a CSE major in 2015, you were part of the chosen ones who could walk into a career fair and walk out with 10+ interview opportunities with companies like Facebook, Google, etc...I myself was a lowly electrical engineering graduate that would try to sneak into CS career fairs for internship opportunities. And inevitably the engineering managers would lose interest or avoid eye contact with me once they found out my true colors.

The CS department had such a chokehold on UW that they managed to squeeze an entire new building out of the administration. Their argument? They simply couldn't produce enough tech workers to meet the industry's insatiable demand. This was the peak of software engineering's golden age.

And it’s crazy how it’s all completely fallen apart.

The Covid Boom and Bust

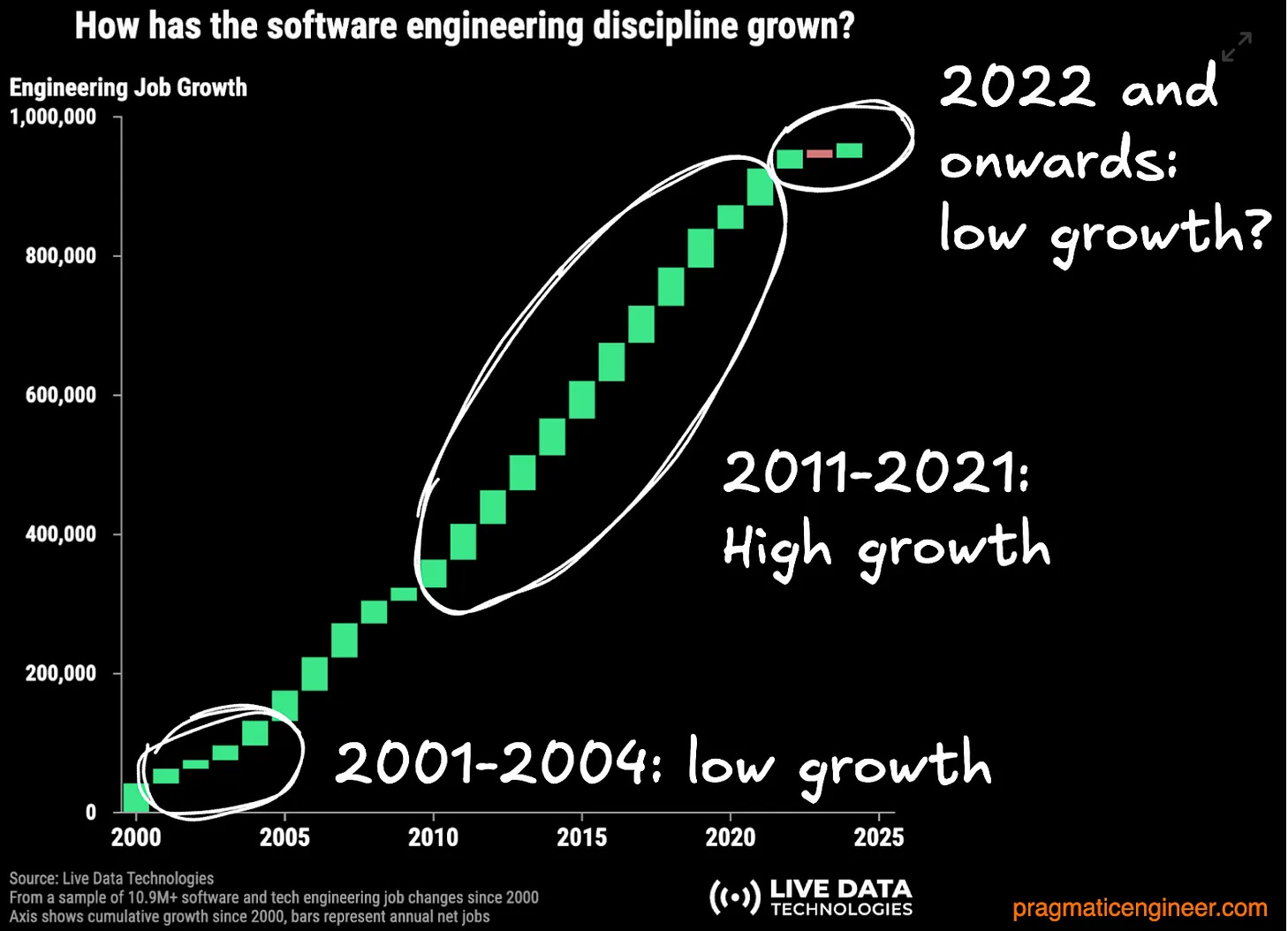

During tech's growth years, the message was clear: learn to code, get a six-figure job. The entire education industry restructured around this promise that the demand for engineers was practically infinite because companies couldn’t hire fast enough. And that’s partially true - look at the growth of software engineering industry from 2000 to 2021.

Naturally, the education market as a lagging indicator also fell in line. From 2015 to 2020, the number of CS university undergraduates doubled from around 60,000 to 100,000 per year. Similarly the number of coding bootcamps graduates since 2016 also tripled from 18,000 to 60,000+ graduates per year.

But then of course, in 2022 and 2023, we saw this little blip in growth as ZIRP and Covid remote education promptly ended and tech layoffs reached an all-time high.

No big deal, one little red blip and we’re back to normal right?

Not exactly. The tech downturn of 2022-2023 rippled through the entire industry, creating the most challenging job market in recent memory. While experienced engineers faced unprecedented layoffs, the entry-level market took the hardest hit. New graduates and career switchers found themselves competing against seasoned professionals who had been laid off, while companies froze or severely reduced their junior hiring pipelines.

This market correction hit coding bootcamps particularly hard, exposing a fundamental weakness in their business model. Unlike universities, which have diverse revenue streams, established endowments, and institutional staying power, bootcamps operate purely as businesses dependent on quick job placements and continued growth.

Career Karma, a platform connecting individuals with coding bootcamps, reduced its workforce by approximately 33%, laying off 60 employees in July 2022 and then again in 2023 before now pivoting their business model to AI companions for education.

Codeup, founded by Michael Girdley, Chris Turner, and Jason Straughan in 2013, ceased operations in late December 2023. The sudden closure left approximately 70-100 students and 20-40 staff members without clear direction

Hack Reactor unexpectedly shut down its part-time program in October 2023.

Bitwise Industries, a tech company offering coding education, furloughed its entire workforce of 900 employees in May 2023 and the founders are facing federal wire fraud charges in excess of $100 million.

Flatiron School, acquired by WeWork in 2017, faced challenges leading to layoffs and program pauses and in November 2019, the school laid off dozens of employees as part of broader cuts at WeWork. Three years later in November 2022 they made additional cuts to programs and stuff. .

App Academy is rumored to be completely shutting down after raising private equity funding and paying out secondaries to it’s founders in 2022.

The speed of the bootcamp collapse wasn't just surprising, it revealed they were businesses built on a houses of cards with flawed contradictions.

First, there was the venture capital trap. Bootcamps, and specifically VC funded bootcamps, clearly could not sustain one or two bad years, never mind any kind of contraction. Zero interest rates and pandemic-driven remote learning created an artificial boom in both tech hiring and online education. With that, bootcamps took VC money promising to be tech companies, not education companies. The difference is crucial: tech companies need exponential growth to satisfy investors, while education companies need consistent outcomes to survive. You can't do both.

Venture funding demanded growth exactly when the market demanded contraction. When Lambda School raised $122 million, they weren't just taking money, they were making a promise to grow at all costs. That promise would come back to haunt them when the tech job market cooled. Unable to deliver on their promised placement rates and growth targets, they were forced to lay off nearly half their staff, rebrand as "Bloom Institute of Technology," and essentially abandon their original mission. Today, they're reportedly still burning through their VC funding while trying to pivot to a completely different business model.

Second, there was the income share agreement (ISA) trap. Everyone saw the obvious problem: strong candidates who could easily land jobs would choose the upfront payment, while weaker candidates gravitated toward ISAs. But the real killer was in the details: bootcamps couldn't ding credit scores when graduates stopped paying, had no real legal framework for collections, and faced massive upfront costs while waiting years for revenue on the payback.

Top it off with looming regulatory threats and consumer confusion about how ISAs even worked, and you had a financial instrument that seemed clever but was fundamentally broken. For more on why it doesn’t work you can read this twitter thread.

Are Master’s Programs Next?

While bootcamps are imploding and university undergraduates are sweating, Master's programs are doing quite well because of their strange incentive structure.

First, they've started tapping into a completely different market: international students. In 2022, international graduate enrollment shot up 21%. And then another 22% in 2023.

Most in-person Master’s programs are 4x as expensive as a bootcamp which speaks to how valuable their visa opportunity program is for international students that make up 70%+ of most specialty master’s programs.

We’ve seen this at Interview Query where we partner with many Master’s in data science and business analytics programs that have seen continued growth through the period. These specialty master’s programs are now the cash cow for universities that have to balance out a budgetary crisis.

My thesis is that as student enrollment grows, budgets for actual outcomes stay more or less the same, and with a weakening job market the placement rates will nose dive. But unlike bootcamps, universities get paid regardless of whether their graduates find jobs.

This creates a mathematical problem that's getting worse by the day. We have record numbers of CS graduates competing with thousands of bootcamp graduates. We have expanding Master's programs pumping out more graduates than ever. So the supply curve feels like it’s going exponential while the demand curve is mostly still linear in tech.

I’m not sure how this is supposed to play out. Most university administrators I talk to are very interested in macroeconomic conditions which is mostly tough to forecast. But it’s relatively hard to bank your program’s overall success to a macroeconomic forecast.

Overall, the market is getting better as it rebounds from the volatility of the highs and lows. But the additional influx of international students is not going away and serving their needs while dealing with a balance of policy changes around visas and a poor macroeconomic situation is quite a headache.

Things to Share

The Pragmatic Engineer shares a deep dive in How GenAI is Reshaping Tech Hiring. Along with a similar FT article, both detail a very interesting new trend as job-seekers start using more and more AI tools to speed up and optimize their job search process. From the FT article: “Human resources software maker Workday reports that the number of global job applications is growing four times faster than job openings.” With more job applications and AI written cover letters, employers are responding with more take-home exams and AI interviewers to try to weed out applicants. At Interview Query we have been testing a partnership with a recruiting company to send all of their applicants AI assessments and decent number of them are clearly cheating. It’s another AI arms race that unfortunately isn’t netting out that much value for either side and where the best alpha, as I repeat to college students, will be going back to non-tech ways of getting jobs like networking and approaching decision makers.

This interview with Stan Druckenmiller gives insight into his investing process and how it’s changed but also his dedication. He’s not into it for the money. To him every day is the same. He wakes up at 4am, immediately checks Bloomberg, reads all the news, goes to work, works all day, finishes at around 8:30pm right after checking Japan, and then immediately goes to bed. From the article: “If they're going in it for the money, they should go elsewhere. There's too many people in the business like me that just love the game and the passion…and they're not going to be able to outwork the people that are passionate in the game.”

Frank Slootman, the now ex-CEO of Snowflake amongst three other very successful companies, wrote a blog post about amping it up back in 2018 that has now turned into a book. It’s an easy to understand theme, and likely turned into a book because of how much that theme needs to be driven into you on a constant basis if you’re running a company. Ironically about how you as a CEO, need to drive it into the team that you’re leading 100% of the time.