How much does it really cost to live rich?

Sharing my rich life template for everyone to try the thought exercise

How much does it cost to live a rich life?

Probably a lot if your concept of a rich life is Ferraris, private jets, and table service.

But after a few seconds of this thought exercise - you’ll slowly realize that your own personal rich life doesn’t comprise of that.

Inspired by Ramit Sethi’s entire life work - I’ve created my own rich life FIRE template to share for anyone else to use.

The goal of the template is to calculate exactly how much I needed to save to live a Rich Life without having to ever worry about finances again.

It’s a thought exercise to create a nest egg “number” to work towards.

Here’s how it works:

Write down what you think your perfect life looks like. Basically on be content with - sort of a Plan A towards having a fulfilling life.

What do you think you actually need to be happy on a day to day basis? Now forecast those costs.

Then write down the expenses you’d need to live that rich life along with the actual dollar cost.

Lastly - sum up your expenses and run FIRE calculations on the 4% rule to see how much it would cost to do so. (This is what the template does for you).

Here’s the link to the template to get started! (Please make a copy and delete my pre-filled example values while trying not to be too judgmental of my numbers lol).

What is FIRE and why should you care?

If you’ve been following me for a while - you’ll know my light obsession with financial independence and retiring early (FIRE).

The 4% rule behind FIRE is a general rule of thumb that is often used by people who are saving for retirement. It is based on the idea that if you withdraw 4% of your savings each year during retirement, your savings should last for at least 30 years.

The 4% rule standardizes that after taxes, inflation, stock market appreciation and downturns, on average you should be able to comfortably live off of 4% of your wealth every single year and have your nest egg either increase slightly or stay the same every year.

It’s great for managing risk for people that are inherently more risk-averse. The math proves that this is possible but some people do believe that the historical returns from the S&P return may not last forever.

There’s also a lot of people that work really hard and get tunnel vision on FIRE instead of realizing that they should be enjoying the journey. There are, a lot, of people, that get depressed when they get rich.

I think the common response is: “Boo hoo, you’re rich now, get over yourself”. But what’s fairly common is that most people spend their lives shooting for FIRE and now are at a loss for meaning in life after spending all their Mana points on generating wealth.

This is exactly what the rich life exercise is supposed to fix.

It’s supposed to be a REALISTIC example of what you’d find yourself happiest with doing once you’re financially free.

You might keep on working. Who knows? It’s a highly personal value based system to see how you can spend your own money.

And I think the best part is that doing this exercise, most people realize they might need less money than they think.

Maybe this inspires you to stop slaving away at a corporate job for years to save millions of dollars? I don’t know I’m speculating here.

How the Rich Life Sheet Works

I’ve added a few customizations on top of the principles of FIRE here that I added to the sheet.

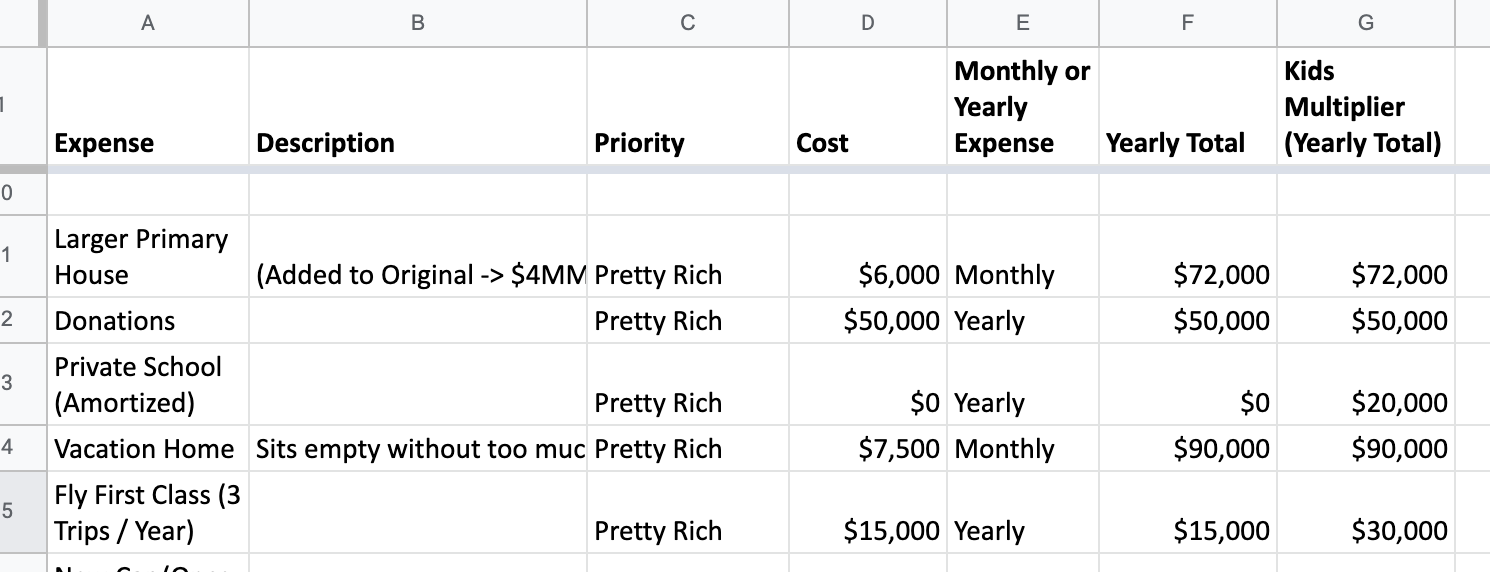

Expenses on the sheet are divided into yearly expenses or monthly expenses.

And as I started working on it - I realized that I wanted to compare different “rich life variants”.

For example - below all the standard rich life line items I added additional options for a “Pretty Rich Life”.

Generally this is helpful for anyone that wants to dream a bit more. It’s partly an exercise of excess on my part, but also lets you see how much you might need to live the life of pure fantasy. And realistically to me this number isn’t as high as most people think.

The goal is that by the end anyone can have a very good model towards different paths they want to take.

Feel free to edit the template as you which. If you want to add in another option for more or less kids that’s completely fine. If you want to add different levels of wealth or even survivor levels (I’ve definitely modeled out how much I need in the worst case scenario of being paraplegic or single and alone).

Ultimately the goal is to cement the thought experiment of what a truly happy and rich life looks like? And in doing so - you might realize that you’re almost there!

Some Common Caveats to Address

Amortizing Expenses and Kids

I’m biased right now because I don’t have kids and I don’t know how much having children cost. I added in my own “Kids Multiplier” column on all expenses that I estimated. Feel free to adjust as you wish.

However, when people complain about the cost of child care and stuff like mortages, they’re concerns are valid - but I feel like most people don’t understand that these expenses eventually go away (unless you’re trying to subsidize your kids into generational wealth of which I can’t help you anymore).

My solution is to amortize many of these costs across a long time frame (generally 30 years).

But wait Jay - a mortgage is 30 years anyway! Yes I know, but then I read this post on Reddit post about how to calculate mortgages into your FIRE. In a TLDR - divide your mortgage in half - maybe less if your interest rate is higher.

Inflation and Lifestyle Creep

While the 4% rule is a reasonable place to start, it doesn't fit every investor's situation. From the same Schwab article I linked before:

It's a rigid rule. The 4% rule assumes you increase your spending every year by the rate of inflation—not on how your portfolio performed—which can be a challenge for some investors.

It also assumes you never have years where you spend more, or less, than the inflation increase. This isn't how most people spend in retirement. Expenses may change from one year to the next, and the amount you spend may change throughout retirement.

So in general I believe it counteracts any fears of inflation unless you believe that inflation will continue to rise above historical averages.

For example - if you believe that the Fed will change and in the future set a 3% target for inflation instead of a 2% target - then you’ll have to adjust your own expectations and probably save more.

That being said - here’s a couple links on if $5 million is enough to retire on.

Twitter debate on if you never need to work again if you had $5 million at 35

Why $5 Million Is Barely Enough To Retire Early With A Family

My opinion? There’s a lot of “necessities” that look more like excess. But hey - I’m not trying to judge someone’s ideal life!

Coast FIRE and Work Freedom

One of my favorite things to look at is always Coast FIRE. Because the number for Coast FIRE always seems more attainable, and in my opinion, is a more likely evaluation for what will happen barring crazy accidents or life events.

Coast FIRE is when you have enough in your retirement accounts that without any additional contributions, your net worth will grow to support retirement at a traditional retirement age.

Once your net worth has passed the Coast FIRE milestone, you still need to earn enough to cover your monthly cost of living, but you no longer need to save money for retirement. If you save up and invest enough money early enough in life, you can allow your existing investments to compound over time and grow to be enough to retire on at a traditional retirement age. This strategy of "Coasting to FIRE" gives you the freedom to pursue a different job that pays less, shift to working part-time, or just have more spending money to enjoy life.

And the best thing is that Coast FIRE numbers are much more achievable.

For example - in my spreadsheet even with Kids - if my total household income can take-home ~$200K/year, my eventual FIRE number goes from $6.5 million to $2.7 million. That’s under the assumption that you can take home on average $200K/year until your retirement age. Of which during that entire period you’re still spending MORE than you’re actually earning ($260K/year according to my sheet).

More than anything, I think this assuages the notion that surprising life events shouldn’t be too worrisome. Yes making $100K or $200K/year will be difficult no matter what for most people. But at least it’s an understanding that your life won’t be crippled once your income < your expenses.

In my lovely opinion, it’s likely that most people will find contributing in capitalistic ways will still be the most fulfilling activities that we do even when we have enough money to not worry about the future.

I’m personally not someone who once FIRED will think that the best use of my time will be working at Starbucks or volunteering at food shelters. For one it’s not as interesting as continuing to find ways to help other people in higher leverage situations.

Let me know your thoughts

What you think of my template. Are there any assumptions that are wildly off? Is there anything you disagree with or resonate with? I’d love to know.

Otherwise - happy dreaming!