Avoiding 10 Years of Market Stagnation

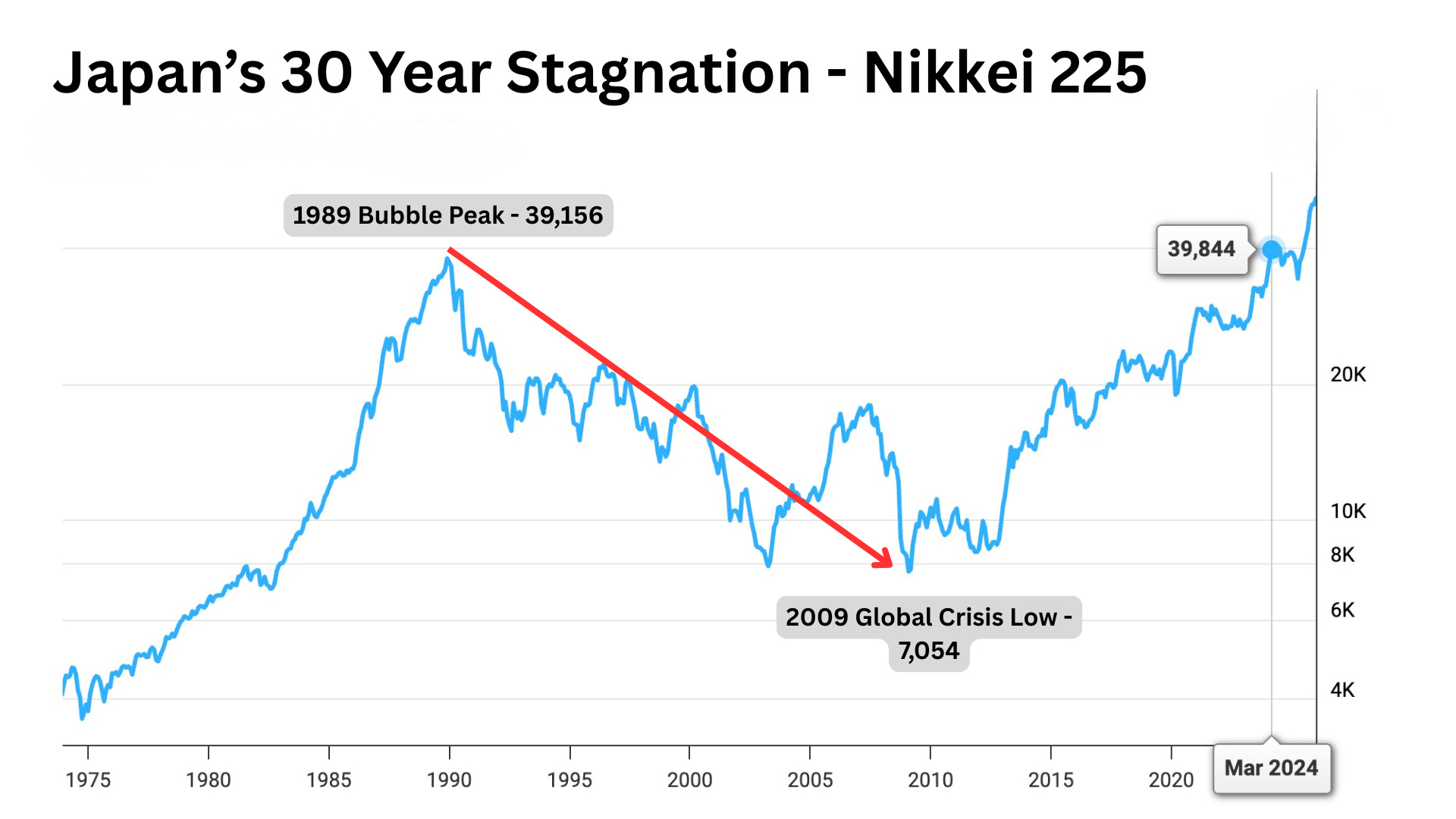

In 1989, Japan was unstoppable. Technology was booming. For a period of 15 years from 1974 to 1989, the Nikkei 225 had gone up over 10x from 3600 to over 39,000.

Sound familiar?

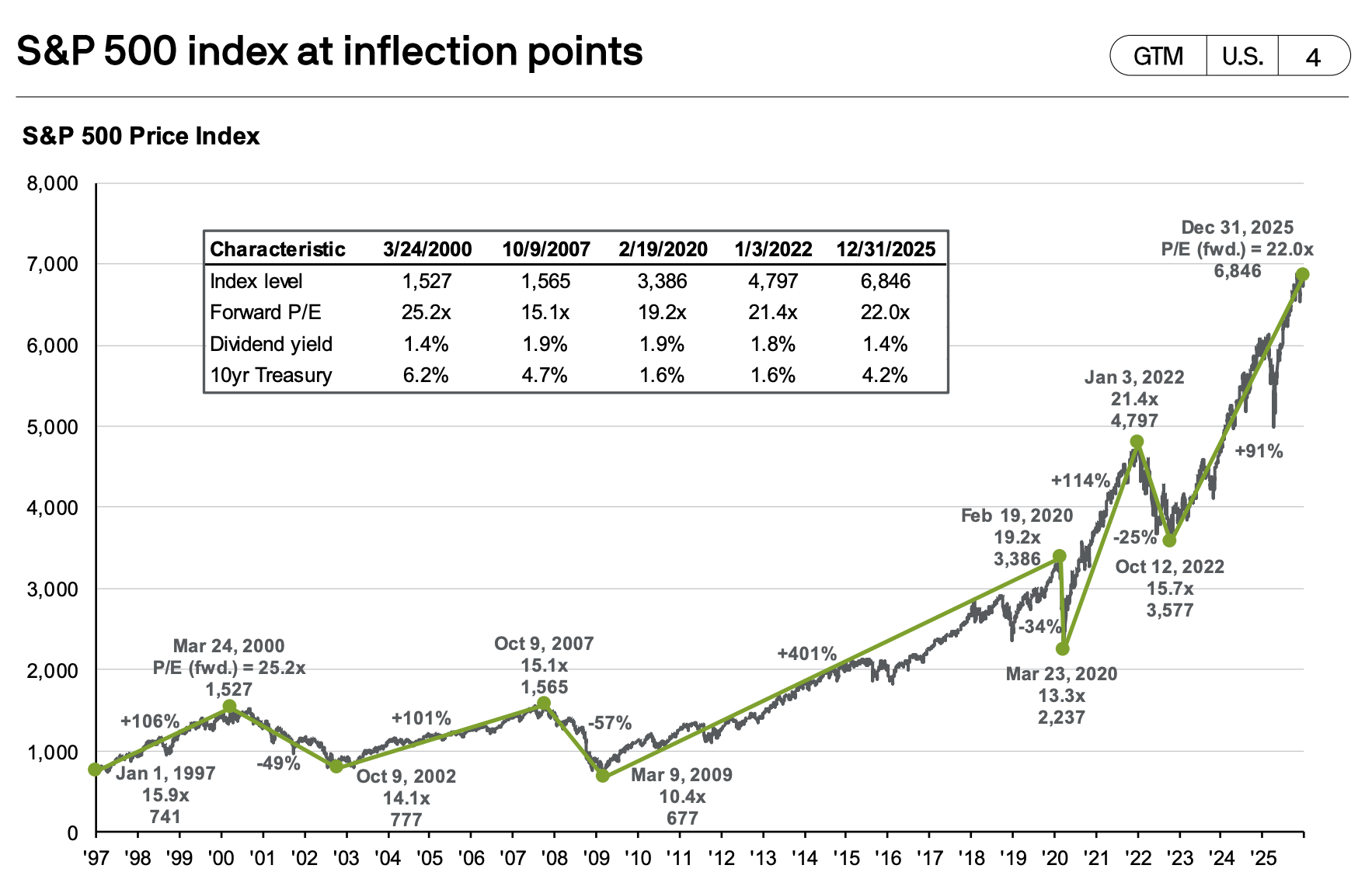

As the S&P 500 continues to reach all time highs, one of the recurring fears is that we are primed for a market correction. The consensus is that we are in an AI bubble and investing now at sky high valuations diminishes returns.

J.P. Morgan released a report last month showing that when investors bought the S&P 500 at forward price to earning (P/E) ratios at around 22x, subsequent 10-year annualized returns have historically ranged between +2% and -2%.

It’s not a guarantee of a crash, but a strong likelihood that returns over the next decade are likely to be “meh”.

Japan is the extreme example. It took almost 35 years later for the Nikkei 225 to finally surpass it’s all-time high index in 1989. But the U.S. has also had multiple periods were real returns were flat: from 2000 to 2012 and 1970 to 1980.

So everyone knows the market is expensive (maybe overvalued?). But nobody is talking about what we’re supposed to do about it.

What are the available options?

There are a few available options. None of them sound that great.

Treasuries & Cash: If you feel like the market is overvalued, you could sell all of your equities and invest in cash or treasury bonds. You lock in 4-5% in interest rates and sleep well. But surprise, after inflation adjustments, you’re looking closer to actually getting 1 to 2% returns. And then there’s the problem of re-timing your entry BACK into the market. What happens to you if the market goes up another 20%?

Buying Gold: Putting your savings into gold or commodities is a strategy used for centuries. From the lost decade from 2000 to 2010, gold’s compound annual growth rate topped 15% while the S&P 500 stayed flat. Similarly in the 1970s, gold soared from $35/ounce to over $850/ounce when the S&P 500 returned an inflation adjusted return of <2%.

So this is the winner right? Not so fast - this requires market timing again similar to treasuries. From 1980 through 1999, gold delivered -6.5% annualized return, compared with 13.3% for the S&P 500. Two decades of losing money while stocks ripped.

International Equities: You can try diversifying internationally. Non-US stocks trade at lower valuations and in 2025 the overall international equities market rose by 30%. The logic is if US valuations are stretched, go where they aren’t. But international markets have been “cheaper” than US markets for over a decade now and anyone who constantly diversified has underperformed. Correlations have also increased so that when the US sneezes everyone catches a cold. You’re diversifying your exposure, but you’re not escaping the system.

Do Nothing: The default advice is then to do nothing, stay invested, and ride it out. And historically it’s been right more often than not. Markets do recover. Time in the market beats timing the market. But “historically” includes a lot of people who waited anywhere from 10 to 30 years for their portfolio to recover.

When we look at the case of Japan, the Nikkei 225 dropped to less than 20% of it’s original peak at one point during the 30 year span of stagnation. Imagine retiring and then watching your net worth hit 1/4 of your original all-time high. How long would you stay in retirement?

Reframing the question

Here’s the thing: is there only one correct decision going forward? In hindsight, there’s always a “correct” trade. But we don’t get hindsight. And even if we did, the right move for one person isn’t the right move for another. We all have different risk tolerances, income levels, and life circumstances. The question isn’t “what will the market do?” It’s “what can my life absorb if I’m wrong?

As Morgan Housel argues in The Psychology of Money: the best portfolio isn’t the one with the highest expected return: it’s the one you can actually stick with when markets drop 30%, 40%, or 50%.

The right decision depends on the combination of market outcomes and your own risk profile. An older person nearing retirement doesn’t have the same relationship to risk as a new college graduate with forty years of income ahead.

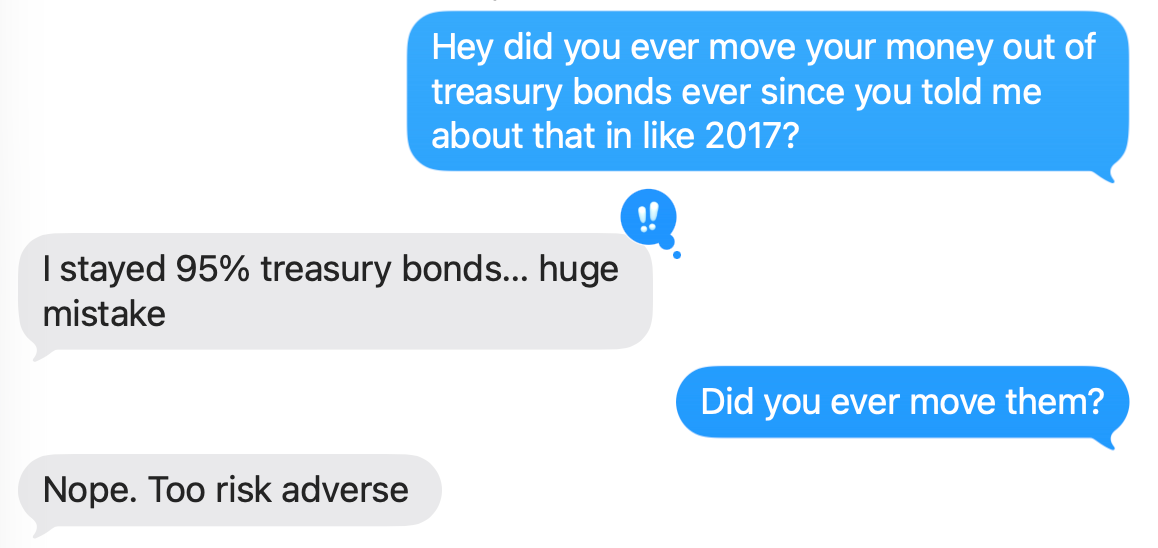

But age isn’t the only factor. A friend of mine in 2017 saw the bull market, believed tech companies were inflating their prices by buying back shares, and moved his entire portfolio over to treasury bonds. He’s missed the S&P 500 roughly tripling since then. But he had also lost his job, had inherited enough to live off of the bonds interest, and genuinely needed that security. For him, it might have been the right call.

What I’m doing

My next ten years look riskier than the last. Future kids, healthcare costs, and a potential career change that could take years to pay off. I’ve started diversifying, not by selling, but allocating new savings into bonds and international equities I had never touched before. For the first time this past year I bought gold.

The framework that I keep coming back to is simple.

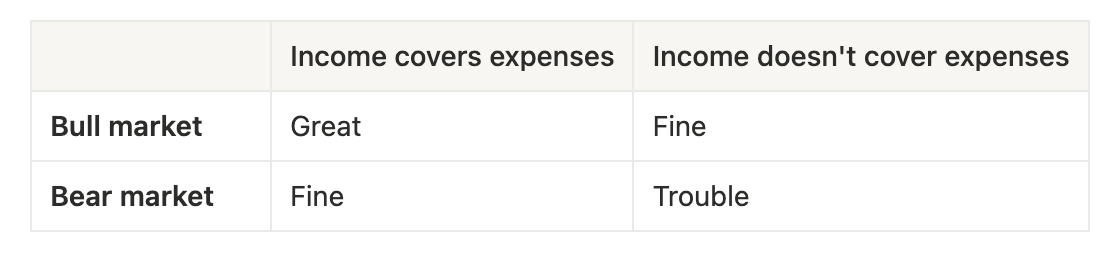

How many years could I survive in the bottom right corner, drawing from my investments while simultaneously watching them shrink? I’ve talked before about freedom and flexibility as a constraint, and I ask myself how much am I willing to pay to protect it.

I also think about how I would feel if I missed out on the market doubling. Would I feel regret? Would the pain of missing a 2x gain hurt more than watching my portfolio drop by half?

When the Japan scenario creeps into my head, I remind myself: even that wasn’t as catastrophic as the headline suggests. Japan in the last 30 years had multiple periods of deflation, which meant that normal everyday items were cheaper as their investments plummeted. And if you had reinvested dividends the whole time, total returns for the Nikkei 225 were +54% (in yen terms) beating out inflation which rose 20% over that period. A lost thirty years is painful. But it’s not the same as losing everything.

History is telling us that there might be mediocre returns for the next decade. But knowing that doesn’t tell you what to do about it. The goal isn’t to predict the market. It’s to build a life that doesn’t depend on the prediction.